If you have been thinking about buying a home or refinancing your mortgage in 2026, you have probably noticed one thing: rates are still frustratingly high. You are not alone in feeling that way. Millions of Americans are in the same boat — waiting, watching, and wondering when things will finally ease up.

In this guide, we will walk you through everything you need to know about mortgage rates in the USA right now — where they stand today, why they are where they are, and what experts think is coming next.

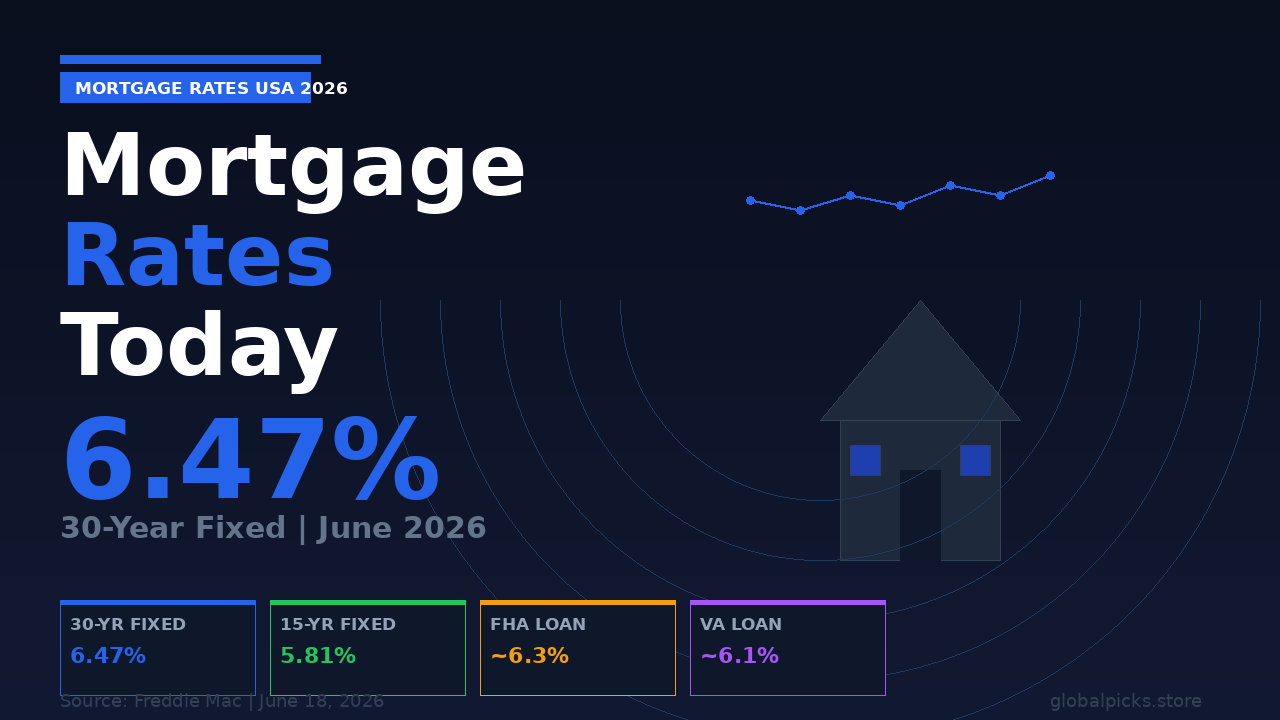

Where Are Mortgage Rates Today? (June 2026)

Let us start with the numbers you actually care about.

<cite index=”3-1″>As of June 18, 2026, the 30-year fixed-rate mortgage averaged 6.47%, down slightly from 6.52% the previous week, according to Freddie Mac. The 15-year fixed-rate mortgage averaged 5.81%.</cite>

Here is a quick snapshot of current rates:

| Loan Type | Current Rate (June 2026) |

|---|---|

| 30-Year Fixed | 6.47% |

| 15-Year Fixed | 5.81% |

| 30-Year FHA Loan | ~6.3% – 6.6% |

| 30-Year VA Loan | ~6.0% – 6.3% |

| 5/1 Adjustable Rate (ARM) | ~5.8% – 6.2% |

<cite index=”2-1″>As of early June 2026, the average rate for a 30-year fixed mortgage is sitting around 6.3% to 6.6%. The good news is this is a bit better than some of the peaks we saw a couple of years ago. The not-so-great news is it is still considerably higher than what many of us got used to before 2022.</cite>

How Did We Get Here? A Quick History

To understand where rates are today, it helps to look back at where they have been.

- 2020-2021: Rates hit historic lows, falling below 3% — an incredible time to buy or refinance

- 2022: Inflation surged and the Federal Reserve started aggressively raising rates

- 2023: The 30-year fixed mortgage hit a 23-year high, peaking close to 7.79%

- 2024: <cite index=”4-1″>The Fed made three rate cuts in September, November, and December 2024 as inflation gradually cooled</cite>

- 2025: <cite index=”4-1″>The Federal Reserve held the federal funds rate steady at its first five meetings, before continued instability and weakened job markets justified three more cuts to end the year</cite>

- 2026: Rates have stabilized in the mid-6% range but remain elevated

<cite index=”4-1″>Mortgage rates fluctuated significantly in 2023, with the average 30-year fixed rate going as low as 6.09% and as high as 7.79%. That range narrowed from 6.08% to 7.22% in 2024, and further in 2025 between 6.15% and 7.04%. So far in 2026, the average 30-year moved between 5.98% and 6.46%.</cite>

Why Are Mortgage Rates Still High in 2026?

This is the question everyone is asking. The Fed has cut rates — so why have mortgage rates not come down more?

Here is the honest answer: mortgage rates and the Fed’s rate are not the same thing.

1. The Middle East Conflict

<cite index=”1-1″>Interest rates have gone up significantly since the U.S. launched its war in Iran at the end of February 2026. As of early June, the average 30-year fixed mortgage rate is about 6.5%, compared to before the war when rates were around 6%. Analysts expect the 30-year fixed mortgage rate to stay between 6% and 6.5% over the next three years.</cite>

<cite index=”7-1″>Although inflation has declined substantially from the peaks experienced in 2022 and 2023, investors remain uncertain about when it will return to the Fed’s official long-term target of 2%, especially with elevated oil prices and the ongoing conflict with Iran.</cite>

2. The Bond Market Drives Mortgage Rates

<cite index=”7-1″>The Fed directly influences the federal funds rate, a short-term interest rate that banks charge one another for overnight loans. Many people assume that mortgage rates move in lockstep with the Fed’s decisions, but in fact they are driven primarily by financial markets.</cite>

In simple terms: when investors are nervous about inflation, they demand higher returns on mortgage-backed securities. That pushes mortgage rates up — regardless of what the Fed does.

3. Government Borrowing and Debt

<cite index=”7-1″>Federal government borrowing is another important factor. The long-term budget outlook by the Congressional Budget Office projects continuing large federal deficits and rising debt levels in the years ahead. When the supply of government bonds increases, investors may require higher yields to absorb that additional supply. And because Treasury yields serve as a benchmark for many different types of borrowing costs throughout the economy, mortgage rates often move with them.</cite>

4. Inflation Is Still a Concern

Even though inflation is much lower than its 2022-2023 peak, it has not fully returned to the Fed’s 2% target. As long as inflation stays sticky, mortgage rates are unlikely to fall significantly.

What Are Experts Saying About Mortgage Rates?

<cite index=”6-1″>The majority of rate-watchers polled by Bankrate expect rates to stay flat in the coming days. Of those polled, 50% say rates will stay rangebound this week, another 38% say rates will rise, and just 13% say rates will drop.</cite>

<cite index=”1-1″>Wells Fargo predicts that mortgage rates bottomed out at 6.18% in the first quarter of 2026 and are expected to increase slightly in subsequent quarters. The bank’s economic group expects 30-year fixed mortgage rates to average 6.23% in 2026 and 6.2% in 2027.</cite>

<cite index=”2-1″>The consensus for the next 90 days (May to July 2026) is for mortgage rates to remain relatively stable — likely in the low-to-mid 6% range, with occasional movements of perhaps 0.2% to 0.5% in either direction. Do not expect a cliff-diving rate scenario, nor a sudden spike, unless something truly unexpected happens in the economy or the world.</cite>

How Are High Rates Affecting Homebuyers?

The impact of elevated mortgage rates on everyday Americans is real and significant.

<cite index=”1-1″>In a May 2026 U.S. News survey, nearly two-thirds of homebuyers (62%) were waiting for mortgage rates to fall before buying a home. However, the same amount (62%) put off buying a home in 2025 because they were waiting for rates to fall — and they did not.</cite>

<cite index=”9-1″>Mortgage applications fell 3.8%, resuming a downward trend after a brief surge the previous week. Refinance applications dropped 4.5%, while applications for home purchase mortgages declined 3.4%.</cite>

This tells us something important: waiting for the “perfect” rate can backfire. Life does not pause for mortgage rates.

Should You Buy a Home Now or Wait?

This is the million-dollar question — literally. Here is a balanced way to think about it:

Reasons to Buy Now:

- Home prices may rise further if rates eventually drop and demand surges

- You can always refinance later if rates fall significantly

- Renting means building someone else’s equity, not yours

- <cite index=”4-1″>Whatever happens, interest rates are still below historical averages. Dating back to April 1971, the fixed 30-year interest rate averaged around 7.8%. So you can still get a good deal, historically speaking — especially if you are a borrower with strong credit.</cite>

Reasons to Wait:

- Rates may ease if inflation cools and geopolitical tensions ease

- Home prices in many markets remain high

- A larger down payment now means less borrowing later

- Your personal financial situation matters most

The honest truth: If you need a home, can afford the payments, and plan to stay for 5+ years — buying now is not a bad decision. If rates drop significantly later, refinancing is always an option.

How to Get the Lowest Mortgage Rate Possible

Regardless of where the market is, you can take steps to secure the best rate available to you:

1. Improve Your Credit Score Lenders reserve the best rates for borrowers with scores above 740. Even a 20-point improvement can save you thousands over the life of a loan.

2. Make a Larger Down Payment Putting down 20% or more eliminates private mortgage insurance (PMI) and often unlocks lower rates.

3. Shop Around — Always <cite index=”2-1″>Always get current quotes from lenders when you are ready to make a move.</cite> Getting quotes from at least 3-5 lenders can save you significantly. Even a 0.25% difference in rate saves thousands over a 30-year loan.

4. Consider a 15-Year Loan If you can afford higher monthly payments, a 15-year fixed mortgage at 5.81% saves you an enormous amount in interest compared to a 30-year loan.

5. Look into ARM Loans <cite index=”2-1″>If you plan to move or refinance in a few years, an adjustable-rate mortgage (ARM) might offer a lower initial rate. Just be aware of the risks when the rate adjusts.</cite>

6. Buy Points Paying discount points upfront lowers your interest rate. This makes sense if you plan to stay in the home long-term.

7. Lock Your Rate Once you find a good rate, lock it in immediately. Rates can change daily — sometimes multiple times a day.

Should You Refinance in 2026?

<cite index=”2-1″>Honestly, unless rates drop by at least 0.75% to 1% below your current rate — and you factor in the closing costs — there is probably not much point in refinancing right now. Keep an eye out for dips, though.</cite>

If you bought your home in 2023 when rates peaked near 7.5-7.79%, you may be in a position to benefit from refinancing now at 6.47%. Run the numbers carefully and factor in closing costs, which typically run 2-5% of the loan amount.

Mortgage Rate Outlook: What to Expect for the Rest of 2026

Looking ahead, here is what the data and experts suggest:

| Period | Expected Rate Range |

|---|---|

| June-July 2026 | 6.3% – 6.6% |

| Q3 2026 | 6.2% – 6.5% |

| Q4 2026 | 6.0% – 6.4% |

| Full Year 2026 Average | ~6.23% |

| 2027 Average | ~6.2% |

<cite index=”1-1″>The short-term direction of rates will be influenced by the geopolitical climate. If the conflict ends, interest rates will have room to move downward. However, rates will stay elevated as long as the war in Iran continues, pushing up oil prices and overall inflation.</cite>

Frequently Asked Questions

Q: What is the average 30-year mortgage rate right now?

A: As of June 18, 2026, the average 30-year fixed mortgage rate is 6.47%, according to Freddie Mac.

Q: Will mortgage rates go down in 2026?

A: Experts expect rates to stay in the 6% to 6.5% range for most of 2026. A significant drop is unlikely unless geopolitical tensions ease and inflation returns to the Fed’s 2% target.

Q: Is 6.47% a good mortgage rate?

A: By historical standards, yes. The long-term average going back to 1971 is around 7.8%. However, compared to the sub-3% rates of 2020-2021, it feels high — and it does make a significant difference in monthly payments.

Q: What credit score do I need for the best mortgage rate?

A: Generally, a credit score of 740 or above will get you the most competitive rates. Scores below 620 may make it difficult to qualify at all.

Q: How much does a 1% difference in mortgage rate matter?

A: On a $400,000 loan, the difference between 5.5% and 6.5% is roughly $250/month — or about $90,000 over the life of a 30-year loan. It matters a lot.

Q: Should I get a fixed or adjustable rate mortgage in 2026?

A: If you plan to stay in your home long-term, a fixed rate gives you stability and protection if rates rise. If you plan to sell or refinance within 5-7 years, an ARM’s lower initial rate may save you money.

Bottom Line

Mortgage rates in 2026 are sitting in the mid-6% range — elevated compared to the historic lows of 2020-2021, but not out of the ordinary by longer-term historical standards.

The biggest factors keeping rates high are geopolitical uncertainty, persistent inflation concerns, and heavy government borrowing. Until those pressures ease, rates are unlikely to fall dramatically.

If you are waiting for rates to drop to 3% again — that is probably not happening anytime soon. But if you are financially ready, have a good credit score, and can afford the payments comfortably — there has never been a bad time to own a home in the long run.

The smartest move is to stay informed, shop around for the best rate, and make a decision based on your personal financial situation — not just the headlines.

Disclaimer: This article is for informational purposes only and does not constitute financial or mortgage advice. Mortgage rates change daily. Please consult with a licensed mortgage professional before making any decisions.

“Ali Murtaza is the founder of Global Picks — a research-driven platform covering legal rights, insurance, finance, and lifestyle topics. He is passionate about making complex information simple and accessible for everyday people.”