Let’s be honest — nobody enjoys paying for insurance. But in 2026, it has become something you really cannot afford to ignore. Rates are shifting across the board: auto, home, health, and life insurance are all seeing changes. Some are going up. Some are actually coming down. And knowing the difference could save you hundreds — or even thousands — of dollars this year.

This guide breaks down exactly what is happening with insurance rates in 2026, why it is happening, and most importantly, what you can do about it right now.

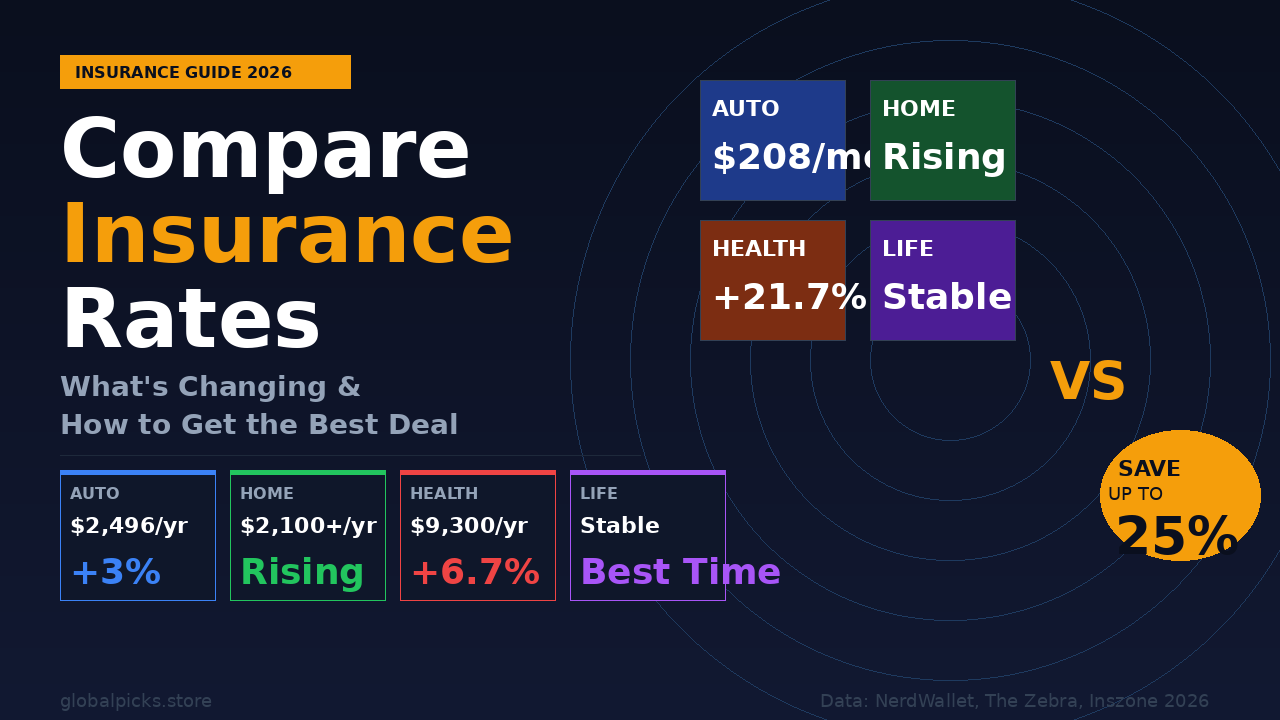

The Big Picture: Where Are Insurance Rates in 2026?

<cite index=”1-1″>Many people saw big jumps in insurance costs throughout 2025. Auto, home, business, and health coverage all became more expensive. As we move into 2026, the picture is mixed. Some lines are calming down, but others are still under pressure.</cite>

Here is a quick snapshot of where each type of insurance stands today:

| Insurance Type | 2026 Trend | Average Annual Cost |

|---|---|---|

| Auto (Full Coverage) | Stabilizing, slight increase | $2,356 – $2,551 |

| Home Insurance | Rising due to climate risk | $2,100 – $3,500+ |

| Health Insurance | Significant increases | $9,300 (single) / $27,000 (family) |

| Life Insurance | Most stable, modest changes | Varies by age/health |

1. Auto Insurance Rates in 2026

What is Happening

The good news for most drivers: the era of shocking double-digit rate hikes may finally be behind us — at least for now.

<cite index=”8-1″>Overall, from 2025 to 2026, insurance prices are rising — but not by nearly as much as in recent years. Nationally, the average increased around 3%, which is a smaller increase than the year before when insurance prices jumped a whopping 18%.</cite>

<cite index=”6-1″>Insurance prices are stabilizing overall for low-risk drivers. While the national average full coverage premium dipped slightly by the end of 2025, that modest relief was mainly concentrated among drivers with clean records. At the same time, minimum coverage premiums rose, signaling that baseline affordability remains a growing challenge even as inflation cools.</cite>

Average Auto Insurance Costs in 2026

<cite index=”10-1″>The average cost of full coverage auto insurance is $208 per month, or about $2,496 per year, in 2026. Nevada, Louisiana, Florida, Connecticut, and Delaware all have average rates of over $300 per month, making them the five most expensive states for car insurance in the country.</cite>

| State Category | Monthly Rate |

|---|---|

| Most Expensive (Nevada) | $335/month |

| Most Expensive (Louisiana) | $327/month |

| Most Expensive (Florida) | $311/month |

| National Average | $208/month |

| Cheapest (Vermont) | $128/month |

| Cheapest (Maine) | $129/month |

Who is Seeing Rate Increases vs Decreases?

<cite index=”6-1″>High-risk drivers are not feeling pricing relief. Premiums increased for drivers whom insurers consider higher risk, including drivers with a DUI, low credit, and teen drivers. Drivers with a DUI experienced the largest price change — a 35% increase. Teen drivers saw rates go up by an average of 17%.</cite>

<cite index=”10-1″>Five of the 10 largest car insurance companies in the U.S. are expected to lower their car insurance rates. Drivers insured with State Farm could see a decrease of around 4% when they renew in 2026. Allstate has the largest estimated rate hike among major companies, but it is a modest increase of just 1.98%.</cite>

EV Insurance in 2026

<cite index=”10-1″>Electric vehicle insurance is getting cheaper in 2026, bringing costs closer to gas-powered vehicles. However, EVs still cost 18% more to insure than gas-powered cars on average — an improvement from 23% more in 2025. Electric cars made by legacy manufacturers like Chevrolet, Honda, and Ford cost about 49% less to insure than those made by EV-only companies like Tesla and Rivian.</cite>

2. Home Insurance Rates in 2026

What is Happening

Home insurance is where things get really serious in 2026.

<cite index=”1-1″>Home insurance is where climate risk shows up most clearly. Research from federal agencies and academics shows that homeowners insurance has become more expensive and, in some areas, harder to obtain.</cite>

Wildfires in the West, hurricanes in the South, and flooding in the Midwest have forced insurers to rethink how they price risk. In some states, major insurers have pulled out entirely, leaving homeowners scrambling for coverage.

New Laws Protecting Homeowners in 2026

States are stepping up to protect consumers. Here are some key changes:

Colorado: <cite index=”4-1″>A new law requires insurers who use a wildfire risk model to share that information with policyholders. Insurers must provide you with your wildfire risk score and the reasons for the score. You should be informed of which mitigation efforts — for example, a fire-resistant roof — will get you a discount, and you have the right to appeal or improve your score.</cite>

Louisiana: <cite index=”4-1″>Under a new state law as of January 1, 2026, Louisiana insurers must prominently display the previous premium when showing the new premium offered at renewal. Louisiana is also tightening notice for home and auto insurance cancellations by doubling the notice period insurers must give when canceling a policy to 60 days, beginning July 1, 2026.</cite>

How to Save on Home Insurance

- Install fire-resistant roofing and storm shutters

- Bundle home and auto insurance (save up to 10-25%)

- Increase your deductible

- Install security systems and smoke detectors

- Ask about loyalty discounts for long-term customers

3. Health Insurance Rates in 2026

What is Happening

Health insurance is where the most dramatic changes are happening in 2026 — and unfortunately, they are mostly not good news.

<cite index=”2-1″>The 2026 ACA marketplace has become unaffordable for millions. Benchmark silver plan premiums rose 21.7%, substantially exceeding the 6-7% increases expected in employer-sponsored plans. Average out-of-pocket premiums for enrolled consumers increased from $113 to $178 monthly — a 58% jump — because federal subsidy enhancements expired.</cite>

<cite index=”1-1″>Consulting firms project another 6-7% increase in average employer health costs in 2026, driven by specialty drugs including GLP-1 medications, higher utilization, and healthcare wage inflation. Even when employers try to absorb some of the increase, many workers will feel the pressure through higher payroll deductions for medical, dental, and vision plans, as well as higher deductibles, co-pays, or out-of-pocket maximums.</cite>

Average Health Insurance Costs in 2026

| Coverage Type | Annual Premium |

|---|---|

| Employer-Sponsored (Single) | ~$9,300 |

| Employer-Sponsored (Family) | ~$27,000 |

| ACA Marketplace (Silver Plan) | ~$178/month (after subsidies) |

| Average Deductible | $3,786 |

How to Save on Health Insurance

- Use your employer’s plan whenever possible — it is usually cheaper

- Check if you qualify for ACA subsidies at healthcare.gov

- Consider an HSA-eligible high-deductible health plan

- Use in-network providers to avoid surprise bills

- Take advantage of free preventive care

4. Life Insurance Rates in 2026

What is Happening

Here is the bright spot: <cite index=”3-1″>life insurance remains the most stable category in 2026, with pricing that is moderate and predictable, tied to age and health.</cite>

If you have been thinking about getting life insurance, 2026 is actually a great time to lock in a rate — especially if you are young and healthy. Rates are not expected to spike significantly anytime soon.

Average Life Insurance Monthly Premiums (30-Year Term)

| Age | $500,000 Coverage |

|---|---|

| 25 years old | $18 – $25/month |

| 35 years old | $22 – $35/month |

| 45 years old | $55 – $90/month |

| 55 years old | $140 – $220/month |

What is Driving Insurance Rate Changes in 2026?

Here are the main forces pushing rates up across all types of insurance:

1. Climate Change and Natural Disasters

More frequent and severe wildfires, hurricanes, and floods mean insurers are paying out more claims than ever. That cost gets passed on to you.

2. Inflation and Repair Costs

Car parts, construction materials, and medical services all cost more than they did five years ago. Higher repair bills mean higher claim payouts, which means higher premiums.

3. AI-Driven Underwriting

<cite index=”3-1″>If 2025 was the year insurers broadly integrated AI, 2026 is the year consumers begin to feel those changes firsthand. Insurers are using AI to sift through vast amounts of data in underwriting, speed claims handling, and power 24/7 chatbots. When done well, it means faster service and more accurate pricing.</cite>

4. Market Competition

<cite index=”2-1″>The auto insurance market is witnessing consolidation pressure. Progressive’s aggressive growth strategy and technology-enabled underwriting have captured market share, while legacy insurers like State Farm raised rates to restore profitability. This competitive dynamic suggests premium increases may moderate for savvy shoppers who compare quotes frequently.</cite>

5. Telematics and Usage-Based Insurance

<cite index=”9-1″>Telematics or usage-based insurance used to feel a bit too “Big Brother” for most folks. Perhaps its time in the mainstream is coming as people are desperate to find any way to bring down insurance premiums in 2026.</cite>

How to Get the Best Insurance Deal in 2026

No matter what type of insurance you are shopping for, these strategies will help you pay less:

1. Shop Around — Every Single Year

This is the single most important thing you can do. <cite index=”6-1″>Drivers who compare multiple providers, consider telematics, reassess coverage levels, and bundle policies are best positioned to manage costs in 2026.</cite> Get at least 3-5 quotes before renewing.

2. Bundle Your Policies

<cite index=”5-1″>One of the best ways to save on insurance is by getting multiple policies with the same company, such as homeowners and car insurance. USAA is the best company for bundling your home and auto policies, followed by Travelers and Progressive.</cite> Bundling typically saves 10-25% on both policies.

3. Try Telematics / Usage-Based Insurance

If you are a safe driver who does not drive much, telematics programs can dramatically lower your premium. Apps track your speed, braking, and mileage — and reward safe behavior with discounts.

4. Improve Your Credit Score

In most states, your credit score directly affects your insurance premium. Improving your score from fair to good can save you hundreds per year.

5. Increase Your Deductible

Raising your deductible from $500 to $1,000 can lower your premium by 10-20%. Just make sure you have enough savings to cover the higher deductible if you need to file a claim.

6. Ask About Every Discount Available

Common discounts include:

- Good driver discount

- Good student discount

- Multi-car discount

- Loyalty discount

- Safety features discount (dashcam, anti-theft device)

- Paperless billing discount

- Pay-in-full discount

7. Review Your Coverage Annually

Your needs change over time. That 10-year-old car probably does not need comprehensive and collision coverage anymore. Dropping unnecessary coverage can save you significantly.

Best Insurance Companies to Compare in 2026

Auto Insurance

| Company | Best For | Avg Monthly (Full) |

|---|---|---|

| USAA | Military families | $124 |

| Travelers | Best overall | $97 |

| GEICO | Cheapest rates | $98 |

| Progressive | High-risk drivers | Above average |

| State Farm | Agent experience | Decreasing ~4% |

Home + Auto Bundle

| Company | Bundle Savings |

|---|---|

| USAA | Up to 10% (military only) |

| Travelers | Up to 13% |

| Progressive | Up to 12% |

| Liberty Mutual | Up to $950/year savings |

| Nationwide | Up to 20% |

Frequently Asked Questions

Q: Are insurance rates going up or down in 2026?

A: It depends on the type of insurance and where you live. Auto insurance is rising modestly (around 3% nationally) after years of double-digit hikes. Health insurance is rising significantly. Life insurance remains stable. Home insurance varies dramatically by state and climate risk.

Q: Which states have the cheapest car insurance in 2026?

A: Vermont ($128/month), Maine ($129/month), and Wyoming ($131/month) have the cheapest full coverage car insurance in the country.

Q: Which states have the most expensive car insurance?

A: Nevada ($335/month), Louisiana ($327/month), and Florida ($311/month) are the priciest states for car insurance in 2026.

Q: How can I lower my insurance rates right now?

A: The fastest ways are: shop around and get multiple quotes, bundle your home and auto policies, sign up for a telematics program if you are a safe driver, and ask your current insurer about every available discount.

Q: Is it worth switching insurance companies in 2026?

A: Absolutely — especially if your rates went up at renewal. Switching can save hundreds per year. Just make sure you are comparing the same coverage levels and check for any cancellation fees with your current provider.

Q: What is usage-based or telematics insurance?

A: It is a type of insurance where an app or device tracks your driving behavior — speed, braking, and mileage — and gives you a discount for safe driving. It can save safe drivers 10-40% on their auto premium.

Bottom Line: What Should You Do Right Now?

The insurance market in 2026 rewards people who pay attention and take action. Here is your simple action plan:

- Right now: Get 3-5 quotes for your auto insurance — use sites like The Zebra, NerdWallet, or Compare.com

- This week: Call your insurer and ask about every discount you qualify for

- This month: Review all your policies — are you over-insured anywhere?

- Bundle: If your home and auto insurance are with different companies, bundle them and save

- Monitor: Set a reminder to compare rates again at your next renewal date

The bottom line is simple: the best insurance deal does not come to you — you have to go find it. But when you do, the savings are real.

Disclaimer: Insurance rates vary based on your personal profile, location, coverage levels, and insurer. Always consult with a licensed insurance professional before making changes to your coverage. Rates mentioned are national averages and your individual rate may differ.

“Ali Murtaza is the founder of Global Picks — a research-driven platform covering legal rights, insurance, finance, and lifestyle topics. He is passionate about making complex information simple and accessible for everyday people.”