When it comes to protecting your family’s financial future, choosing the right insurance policy is one of the most important decisions you will ever make. Two of the most popular options are Life Insurance and Term Insurance. But what is the difference between them? Which one should you choose?

In this comprehensive guide, we will break down everything you need to know about Life Insurance vs Term Insurance — costs, benefits, drawbacks, and which one is best for your situation.

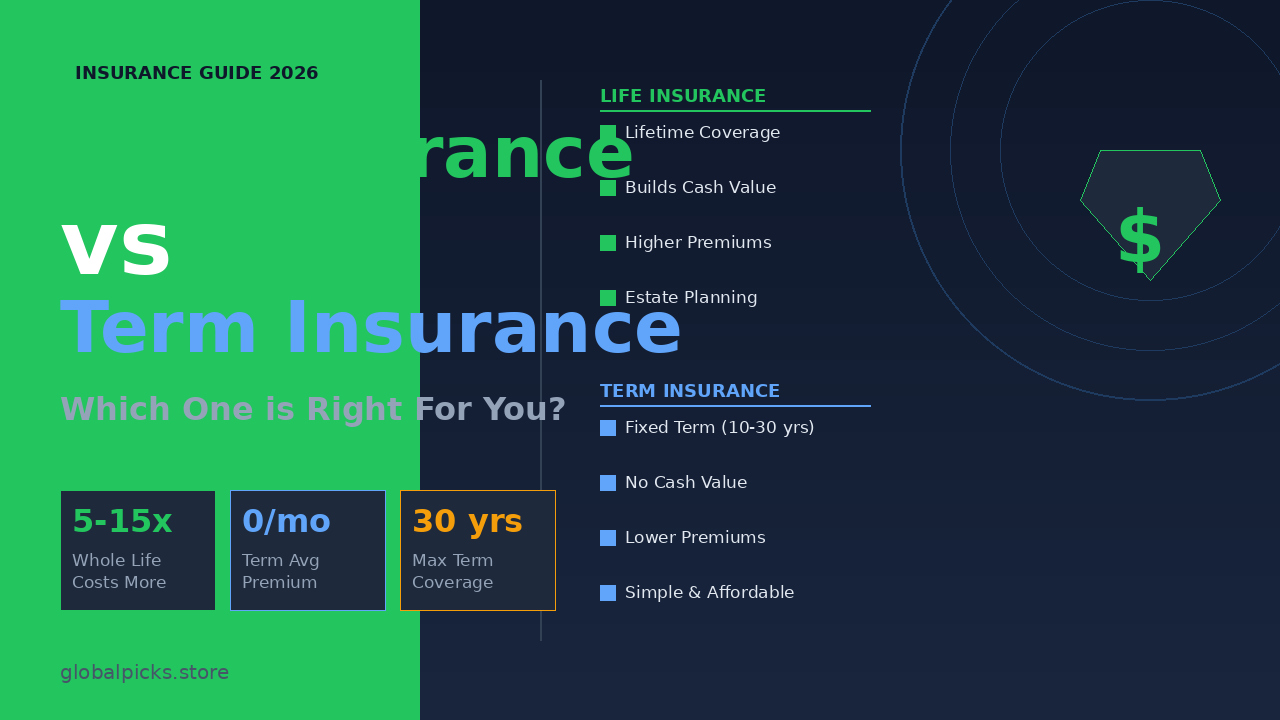

What is Life Insurance?

Life Insurance, also known as Whole Life Insurance or Permanent Life Insurance, is a policy that provides coverage for your entire lifetime — as long as you keep paying the premiums.

Unlike term insurance, whole life insurance does not expire. It also builds a cash value over time, which you can borrow against or withdraw if needed.

Key Features of Life Insurance:

- Coverage lasts your entire life

- Builds cash value over time

- Premiums are fixed and do not increase with age

- Can be used as an investment tool

- More expensive than term insurance

- Death benefit is guaranteed

What is Term Insurance?

Term Insurance is a type of life insurance that provides coverage for a specific period of time — usually 10, 20, or 30 years. If you die within the term, your beneficiaries receive the death benefit. If the term expires and you are still alive, the coverage ends.

Term insurance is the most affordable type of life insurance available.

Key Features of Term Insurance:

- Coverage lasts for a fixed term (10, 20, 30 years)

- No cash value is built

- Premiums are lower than whole life insurance

- Simple and easy to understand

- Ideal for young families and people on a budget

- Coverage ends when the term expires

Life Insurance vs Term Insurance: Key Differences

| Feature | Life Insurance (Whole) | Term Insurance |

|---|---|---|

| Coverage Duration | Entire lifetime | Fixed period (10-30 years) |

| Premiums | Higher | Lower |

| Cash Value | Yes | No |

| Death Benefit | Guaranteed | Only if death occurs in term |

| Best For | Wealth building, estate planning | Income replacement, young families |

| Complexity | More complex | Simple and straightforward |

| Cost | 5-15x more expensive | Very affordable |

| Investment Component | Yes | No |

How Much Does Each Type Cost?

Term Insurance Costs (Average Monthly Premiums):

| Age | Coverage Amount | Monthly Premium |

|---|---|---|

| 25 years | $500,000 | $20 – $30 |

| 35 years | $500,000 | $25 – $40 |

| 45 years | $500,000 | $60 – $100 |

| 55 years | $500,000 | $150 – $250 |

Whole Life Insurance Costs (Average Monthly Premiums):

| Age | Coverage Amount | Monthly Premium |

|---|---|---|

| 25 years | $500,000 | $300 – $500 |

| 35 years | $500,000 | $450 – $700 |

| 45 years | $500,000 | $700 – $1,200 |

| 55 years | $500,000 | $1,200 – $2,000 |

As you can see, term insurance is significantly cheaper than whole life insurance — especially for younger buyers.

Pros and Cons of Life Insurance (Whole Life)

✅ Pros:

- Lifetime coverage — never expires

- Cash value accumulation — grows tax-deferred

- Fixed premiums — never increase with age

- Estate planning tool — great for leaving wealth to heirs

- Loan option — borrow against cash value if needed

- Dividends — some policies pay annual dividends

❌ Cons:

- Very expensive — 5 to 15 times more costly than term

- Complex — harder to understand

- Low returns — cash value grows slowly compared to other investments

- Not ideal for budget-conscious buyers

- Surrender charges — penalties for canceling early

Pros and Cons of Term Insurance

✅ Pros:

- Very affordable — lowest premiums available

- Simple — easy to understand

- High coverage amounts — get $1 million+ coverage cheaply

- Perfect for young families — protect your kids and spouse

- Flexible terms — choose 10, 20, or 30 years

- Convertible — many policies can be converted to whole life later

❌ Cons:

- Expires — no benefit if you outlive the term

- No cash value — premiums do not build any savings

- Premiums increase — if you renew after term expires

- No lifetime protection — not permanent coverage

Who Should Choose Life Insurance (Whole Life)?

Whole life insurance is best for people who:

- Want permanent lifetime coverage

- Have high income and want to build cash value

- Need insurance for estate planning purposes

- Want to leave a guaranteed inheritance to their children

- Are business owners who need key person insurance

- Have dependents with special needs who will need lifelong support

- Have already maxed out other retirement accounts (401k, IRA)

Who Should Choose Term Insurance?

Term insurance is best for people who:

- Are young and healthy and want maximum coverage at low cost

- Have a mortgage they want to protect

- Want to cover their working years (20-30 years) only

- Have young children who need financial protection

- Are on a tight budget but need solid coverage

- Want the simplest form of life insurance

- Plan to invest the difference in savings or retirement accounts

The “Buy Term and Invest the Difference” Strategy

Many financial experts recommend buying term insurance and investing the money you save on premiums in a low-cost index fund or retirement account.

Example:

- Whole life insurance: $500/month

- Term insurance: $30/month

- Difference: $470/month

If you invest $470/month in an index fund earning 8% annually for 30 years, you could accumulate over $700,000 in wealth — far more than the cash value of most whole life policies.

This strategy works best for disciplined savers who will actually invest the difference consistently.

Can You Have Both Life Insurance and Term Insurance?

Yes! Many people choose to have both types of insurance for different purposes:

- Term insurance to cover their family’s immediate needs (mortgage, children’s education, income replacement)

- Whole life insurance for estate planning and permanent coverage

This combination gives you both affordable coverage now and permanent protection later.

Top Life Insurance Companies in the USA (2026)

| Company | Best For | AM Best Rating |

|---|---|---|

| Northwestern Mutual | Whole life, dividends | A++ |

| New York Life | Whole life, term | A++ |

| MassMutual | Whole life, disability | A++ |

| State Farm | Term and whole life | A++ |

| Prudential | Term insurance | A+ |

| Banner Life | Affordable term | A+ |

| Haven Life | Online term insurance | A++ |

| Pacific Life | Universal life | A+ |

How to Choose the Right Policy

Follow these steps to find the right insurance for you:

- Calculate your coverage needs — multiply your annual income by 10-12 times

- Set your budget — how much can you afford monthly?

- Determine your timeline — do you need coverage for 20 years or your entire life?

- Compare quotes — always get at least 3 quotes from different companies

- Check the company’s financial rating — always choose A-rated companies

- Work with a licensed agent — get professional advice before buying

- Review your policy annually — your needs change over time

Frequently Asked Questions (FAQs)

Q: Is term insurance worth it?

A: Yes, term insurance is one of the best financial decisions you can make, especially if you have dependents. It provides maximum coverage at minimum cost during your most important earning years.

Q: Can term insurance be converted to whole life?

A: Yes, many term policies include a conversion option that allows you to convert to whole life without a medical exam. Check your policy for conversion deadlines.

Q: What happens if I outlive my term insurance?

A: If you outlive your term, coverage simply ends. You can renew the policy (usually at higher rates), buy a new policy, or convert it to whole life insurance.

Q: Is whole life insurance a good investment?

A: Whole life insurance is not the best pure investment, as returns are typically low (2-4%). However, it offers unique benefits like guaranteed growth, tax advantages, and lifetime coverage that make it valuable for certain financial situations.

Q: How much life insurance do I need?

A: A common rule of thumb is 10-12 times your annual income. For example, if you earn $60,000/year, you should have $600,000 to $720,000 in coverage.

Q: At what age should I buy life insurance?

A: The younger you buy, the cheaper it is. Ideally, buy life insurance in your 20s or 30s when premiums are lowest and you are in good health.

Final Verdict: Which is Better — Life Insurance or Term Insurance?

For most people, term insurance is the better choice because:

- It is far more affordable

- It provides high coverage during your most important years

- The savings can be invested for better returns

- It is simple and easy to understand

However, whole life insurance makes sense if you:

- Need permanent lifetime coverage

- Want to use it as part of an estate plan

- Have a high income and want tax-advantaged cash value growth

The best insurance is the one you can afford and will actually keep. A $1 million term policy is far better than a $100,000 whole life policy you cancel after 5 years because premiums are too high.

Conclusion

Both Life Insurance and Term Insurance serve important purposes. The key is understanding your financial goals, budget, and coverage needs before making a decision.

If you are young, have a family, and want maximum protection at minimum cost — choose term insurance.

If you want lifelong coverage, have a higher budget, and want to build cash value — consider whole life insurance.

Whatever you choose, do not wait — the younger and healthier you are when you buy life insurance, the lower your premiums will be.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Please consult with a licensed insurance professional before making any insurance decisions.

“Ali Murtaza is the founder of Global Picks — a research-driven platform covering legal rights, insurance, finance, and lifestyle topics. He is passionate about making complex information simple and accessible for everyday people.”